No one particularly enjoys the idea of car insurance. It costs too much, you never get all the coverage you want, and it’s mandatory. Although you might not want to take the time to understand car insurance, it’s important that you do. You need to understand what you’re paying for, why you’re paying for it, and how it can help you in the event of an accident.

Our guide is here to make things a little easier. We’ll discuss the different types of car insurance, where to find it, how to read your policy, and more.

Without further ado, let’s get started!

What Are The Different Types Of Car Insurance?

Comprehensive

The most commonly known type of car insurance, comprehensive coverage covers you in the event of the following:

- Theft

- Vandalism

- Fire

- Natural disaster

- Falling objects

- Damage done by an animal

- Civil disturbances (aka, any damage that may be done during a riot)

As you can see, there are some major things missing, such as coverage for damage from a collision and medical bills you might get from an accident.

That’s because, despite being called “comprehensive,” comprehensive insurance won’t cover everything and you should add some other types of insurance (see below) to your policy.

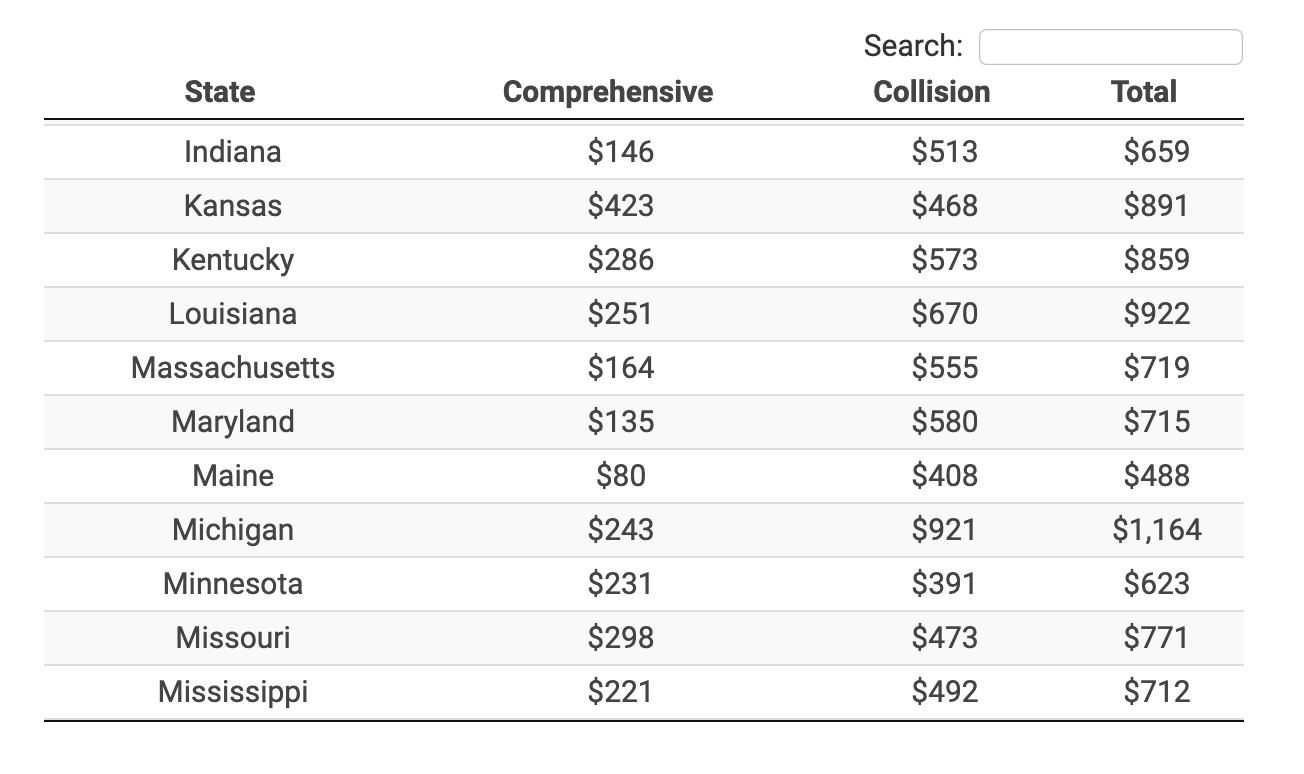

The cost of comprehensive insurance depends on many factors (age, driving record, your car, etc.). But, you can find your state’s average using insurance.com.

Here’s a screenshot of a few different states:

My home state of Maine has a surprisingly low average of just $80 for comprehensive insurance.

Liability

Liability coverage covers your costs when you cause an accident and must pay medical bills and other expenses incurred by the victim of your accident.

The cost of liability insurance, like any other auto insurance, varies due to a lot of factors. But Policygenius found the averages of all 50 states. Here’s a few:

Collision

Collision insurance is exactly what it sounds like–you’re covered if your vehicle collides with another car or object and you need to repair or replace your car.

This is the most expensive auto insurance policy. If you take another look at the chart in the comprehensive insurance section, you’ll see some examples of the high cost of collision insurance.

While comprehensive insurance was, on average, just $80 in my state, collision was an average of $408 per year.

Collision is typically required if you lease or finance a car.

Uninsured/Underinsured

Uninsured/underinsured insurance is an add-on to your typical policy. It covers you in the event that you get into an accident with someone who doesn’t have insurance or doesn’t have insurance that will cover the damage to your vehicle.

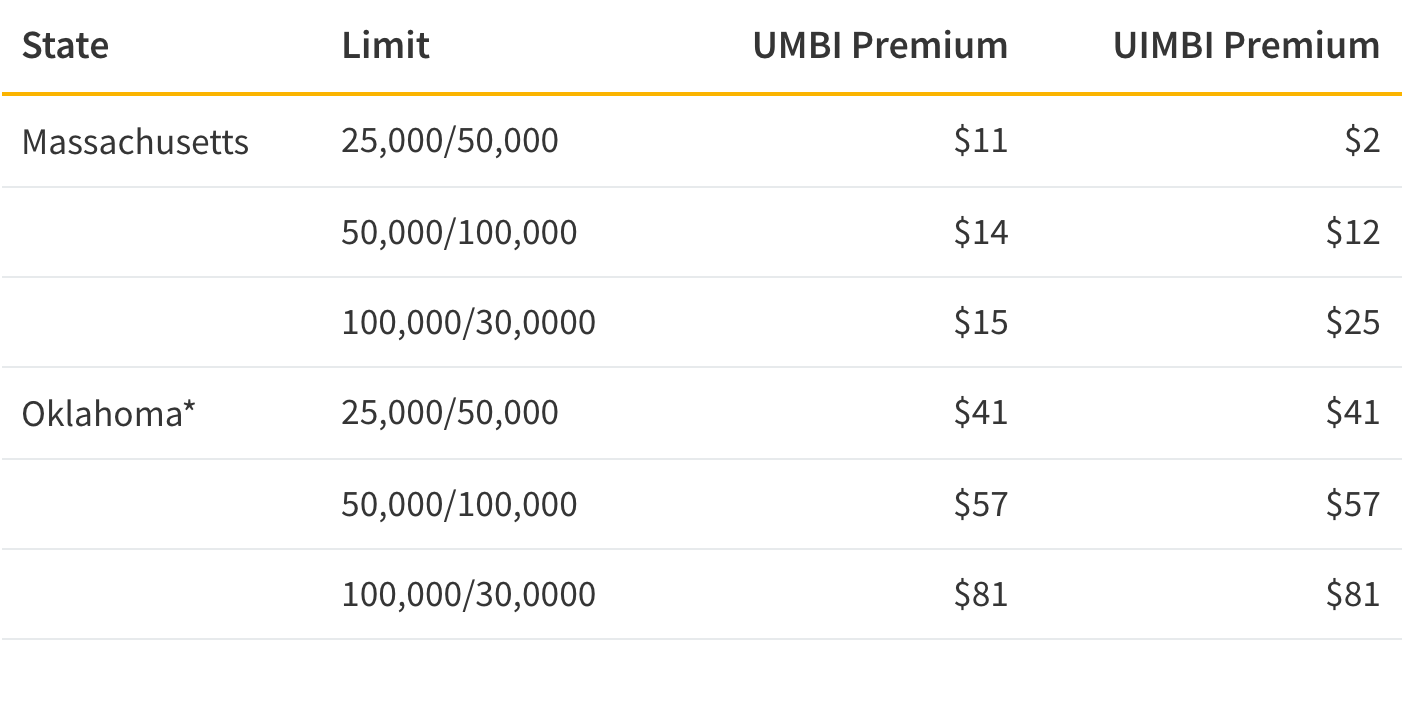

Uninsured is definitely one of the cheaper add-ons for car insurance. ValuePenguin offers the average for the least expensive state (Mass.) and the most expensive state (Oklahoma):

Even Oklahoma, which has the highest amount of uninsured drivers (hence the high cost), only costs $41 per year for the lower end of coverage.

Gap

Gap insurance is for those who lease their car, or those who have taken out a loan to pay for their car. If your car is totaled or stolen, gap insurance will pay the difference (or gap) between what you owe and what your car is worth. For example, let’s say you owe $10,000 on a car that is worth $8,500. If your car is hit and the cost to repair the damages is $9,000, the insurance company will consider your car “totaled” and will pay out the value of the car, or $8,500. This will leave you on the hook for $1,500 that you still owe the financing company.

Gap insurance will step in and pay the extra $1,500 to pay off the car note.

Gap insurance is one of the cheapest auto insurance types, typically costing just a few dollars per month! Worth considering if you owe more than your car is worth.

What Should I Look For When Buying Car Insurance?

Premiums

Your premium is how much you’ll pay for whichever type of policy you choose (i.e. comprehensive, collision, liability, etc.). This is one of the most important factors when deciding on car insurance.

The big-name car insurance companies often have similar premiums for comparable plans and vary by only a few dollars. That’s why we recommend using an insurance aggregator that can show you all your premiums in one place. Compare.com is our favorite (more on this below).

Discounts

Even if some companies have higher premiums, if you’re eligible for discounts, that may not matter too much.

For example, I use Allstate, which is often pricier than other car insurance. However, I qualify for six discounts that drop my monthly cost by about $30.

Deductibles

Similar to a health insurance deductible, an auto insurance deductible is how much you pay after an accident. The insurance company pays the rest.

Unlike health insurance, however, you can’t reach a deductible limit where the insurance company pays everything else going forward. You’ll need to pay a deductible every time you make a claim.

Deductibles typically come with comprehensive and collision insurance. When you increase your deductible, you decrease your monthly payment. But that also means you’ll pay more in the event of an accident.

What Exactly Will Your Insurance Cover?

Many folks get comprehensive car insurance thinking it will cover every instance. Then, after an accident, they find out that they’ll have to pay out of pocket for a new car and their medical bills. It’s frustrating, and not something you want to deal with while recovering from an accident.

This is exactly why it’s vital to understand exactly what you’re getting on your car insurance policy.

Where To Find Car Insurance

Compare.com

Compare.com is an insurance aggregator that shows you all of your rates in one place. They should be your first stop when looking for insurance because it really doesn’t get much easier then Compare.com.

All you have to do is input your ZIP code. Then you can choose to get a quote or simply see a list of all the insurance companies in your area.

Compare.com is completely free, so there’s no harm in using it to see if you can save on your car insurance.

Other Auto Insurance Aggregators

Policygenius

Policygenius works in much the same way as Compare.com. You answer a few basic questions and you’ll get quotes from multiple companies all in one place.

In my experience, Compare works much better than Policygenius. I actually received quotes from Compare, while Policygenius said they would email me my quotes and never did.

Insurify

Insurify is another insurance aggregator that shows all your quotes in one place. They also show all of your eligible discounts in one place, making it easy to compare apples to apples.

They work with some top insurance companies, but they don’t have as many partners as Compare.com.

Allstate

Allstate is a big name in car insurance. They pride themselves on being a part of their communities, and often have local representatives you can speak with face-to-face. I use Allstate and I’ve known my representative since I was 17 and first got insurance.

Allstate is often one of the pricier insurance companies, but their discounts more than make up for it.

GEICO

Everyone knows GEICO for their commercials. However, they’re one of the more expensive car insurance companies, even though they market themselves as low-cost.

Where they do shine is their bundles (combining different types of insurance–home, auto–into one package). You’ll qualify for a much lower rate if you have multiple types of insurance through GEICO

Plus, if you want an insurance company that makes it incredibly easy to use their site and app, GEICO is for you.

Metromile–Your Cheapest Options

Metromile is meant for those who don’t drive that often. It’s a pay-per-mile insurance with a low rate starting at just $29. You’ll pay per-mile after that.

Metromile offers many traditional types of car insurance, including:

- Liability

- Personal injury protection

- Comprehensive

- Collision

Check out our full review of Metromile here.

How To Switch Car Insurance Companies

Step 1: Look At Your Own Policy To Determine What You Actually Have

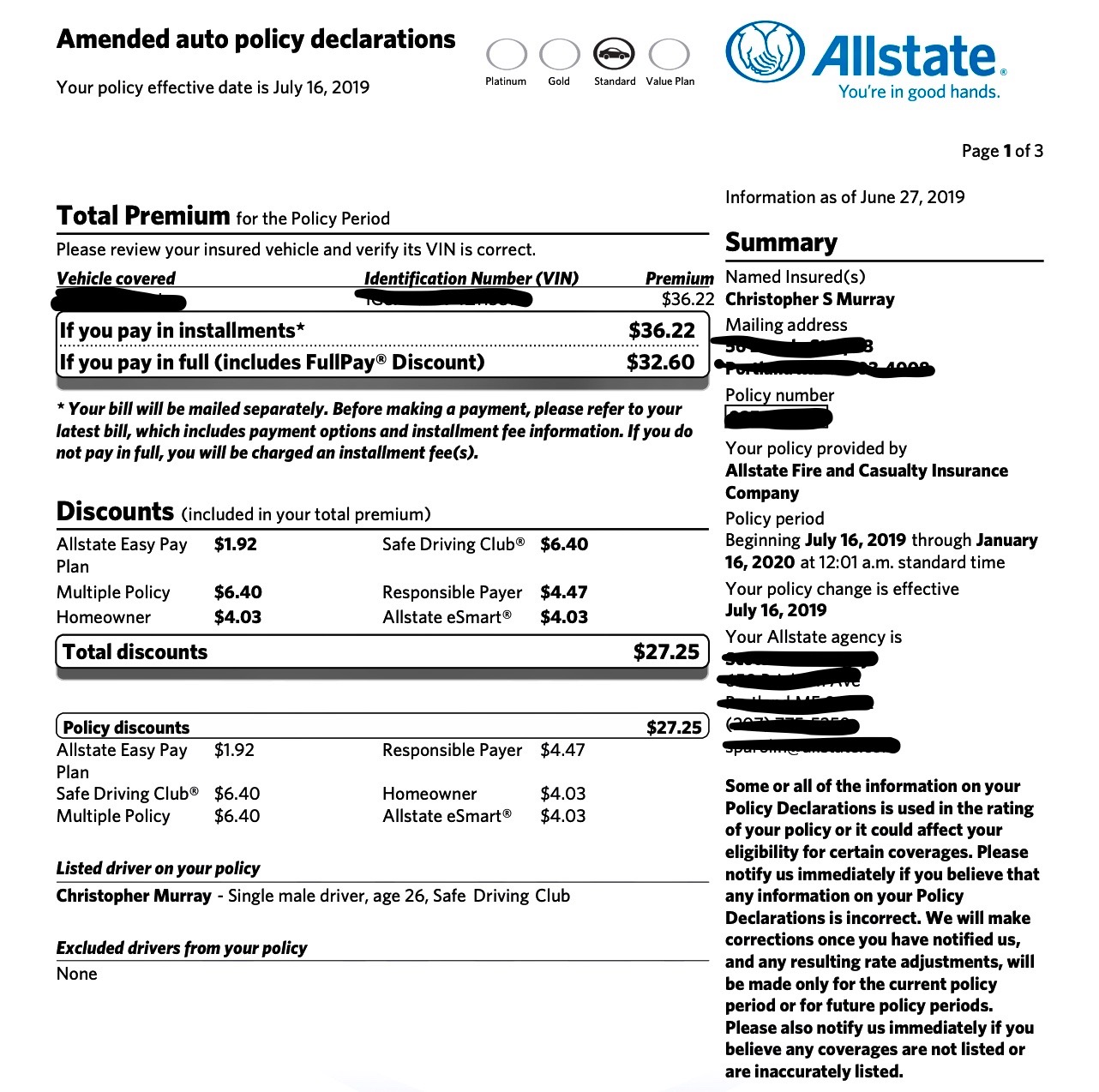

This is the hardest step of the whole process. To help describe how to read your policy, I use my own Allstate policy as an example.

A quick note: I have an odd policy because I’m in between cars. In order to keep my homeowner’s insurance bundled, I needed a replacement policy after selling my car. As a result, my representative suggested I get a policy for cars that spend most of the year sitting in the garage.

With that, let’s get started!

Premium

Let’s start with the premium. A premium is how much you’ll pay for the policy you choose. Allstate lets me choose if I want to pay in full or monthly.

Again, since I have an odd insurance policy right now, it doesn’t matter which one I choose, since they’re only a few cents off. But in the past, the pay-in-full discount has been significant–almost $100.

Policy Period

The policy period is how long you have your policy for. Typically, your policy will last one year. If you look in the right-hand column of my policy, you’ll see that’s exactly how long my policy will last.

Discounts

This is the fun part of your policy. This is also where you’ll want to do some major comparison when choosing a car insurance company. Most car insurance companies are upfront with the discounts they offer; I’m lucky enough to work with a company that automatically applies any discounts they find.

I qualified for the following discounts with Allstate:

- Responsible payer–meaning I paid my bill on time each month

- Easy Pay plan–I have auto-pay set up each month, and Allstate rewards me for that

- Safe Driving Club®–I’ve never made a claim, been in an accident, or gotten a ticket, so Allstate automatically gives me this discount

- eSmart®–I’ve gone paperless, so I get all my bills online

- Multiple policy–I also have homeowner’s insurance through Allstate, so I get a discount for bundling

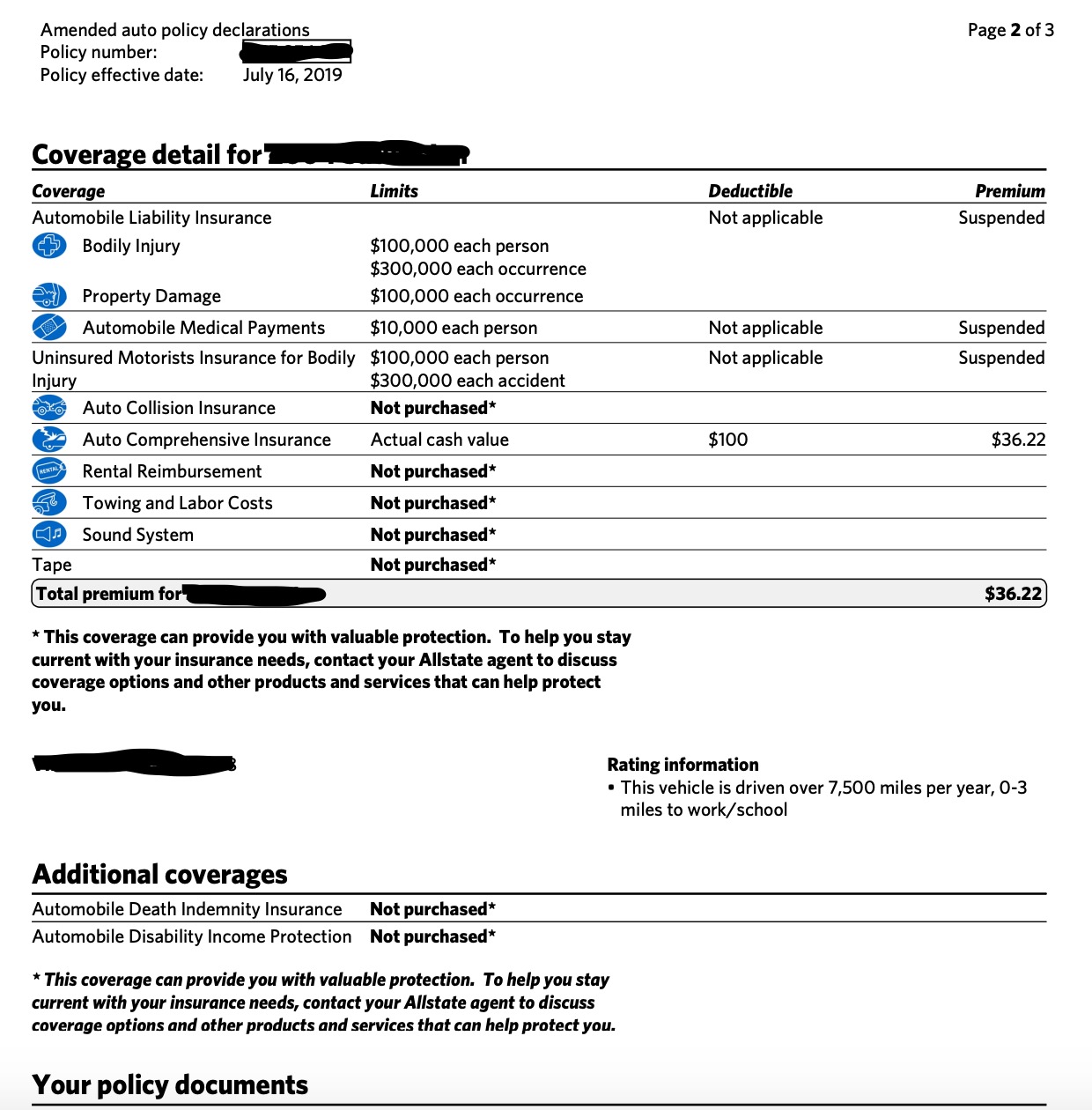

Coverage Details

Now we get into the nitty-gritty of the policy. I have the bare minimum policy, so mine isn’t the best example, but I’ll work with what I’ve got.

Allstate makes it easy to see what I have coverage for. I used to have liability insurance only, which included:

- Bodily injury–I was insured up to $100,000 per person involved in the accident (up to $300,000 per occurrence)

- Property damage–I was insured up to $100,000 for each accident

- Automobile medical payments–If I caused an accident, my insurance covered $10,000 in medical expenses of each person in the car that was hit (not my car)

- Uninsured motorist insurance–If someone else hit me, I was insured for $100,000 for each person (up to $300,000 per occurrence)

This is for a liability policy, meaning it only applies to the other car involved in the accident. I would have had to purchase additional insurance to cover my own vehicle.

Additional Coverages

In the past, I did have additional types of coverage, including:

- Automobile Death Indemnity Insurance–This covers any funeral expenses in the event that you or someone in your vehicle is killed, and the driver of your vehicle is at fault

- Automobile Disability Income Protection–In the event of an accident, this insurance can help cover mortgage payments, personal assistance, groceries, car payments, and more

Step 2: Decide What You Want From Your Insurance

Are you just looking for a lower rate? Do you want more discounts? Better customer service?

What you need is up to you. Once you know what you’re looking for, it will be much easier to narrow down the companies you’re considering.

Step 3: Use Compare.com To Learn How Much You Can Save

Once you know what you’re looking for, go to Compare.com and start comparing rates. Compare is really the best place to start when looking for new insurance.

I decided to give them a try since I’m thinking of switching insurance companies. So let’s go step-by-step through the process.

After I entered my ZIP code, Compare asked me to tell then about my vehicle. I drive a 2004 Dodge Caravan.

Next, Compare asked me a little bit more about my vehicle. I believe in never having an auto loan, so I own my car completely. I’ve also had it for 10 years and, since I work from home, I use my car mostly for personal reasons.

Next, I had to give personal details about myself. Compare asked basic questions like my birthday, name, etc.

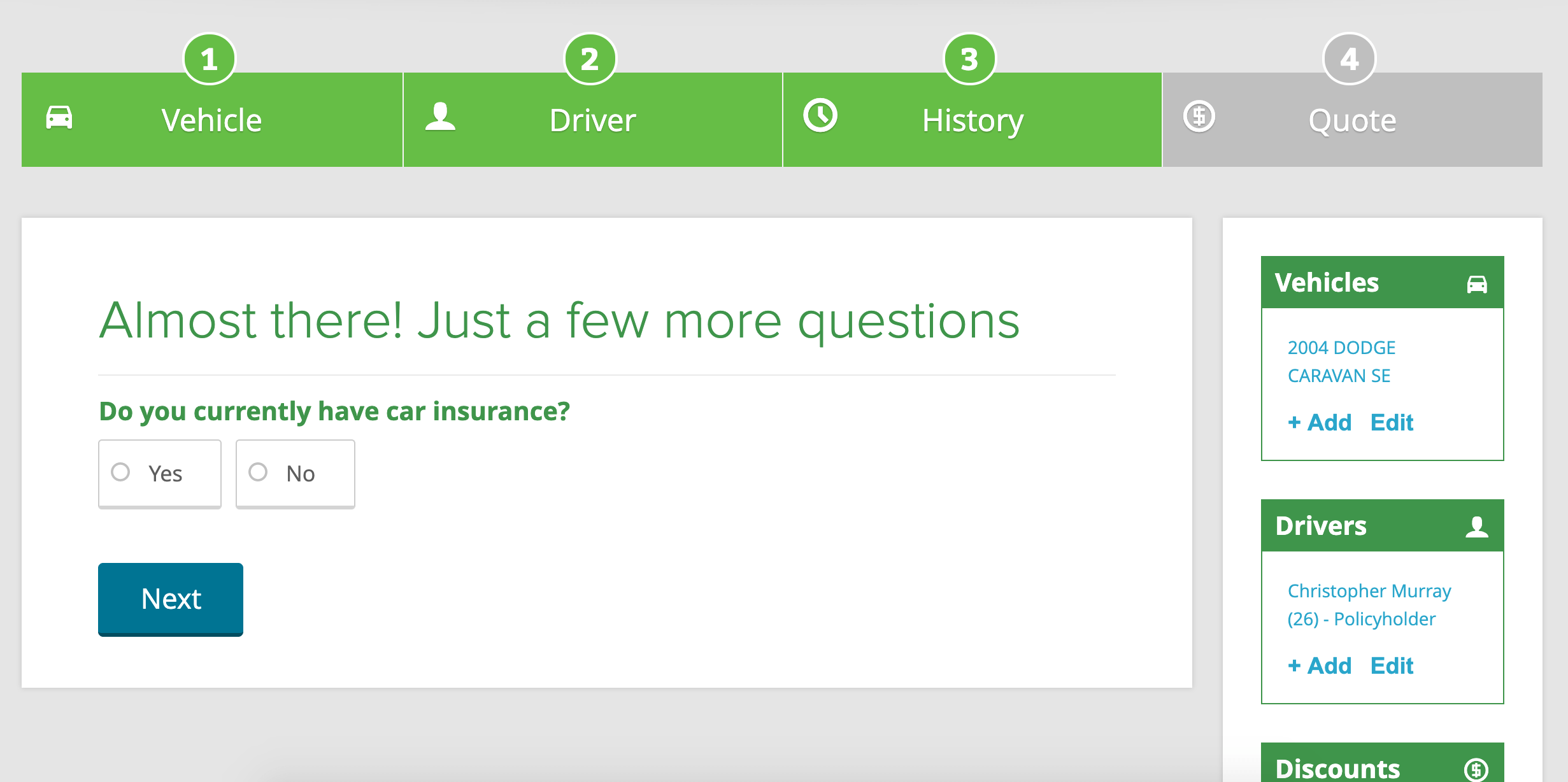

Compare asked me if I currently have insurance, so I answered yes. It then asked me what company I use, and I put Allstate.

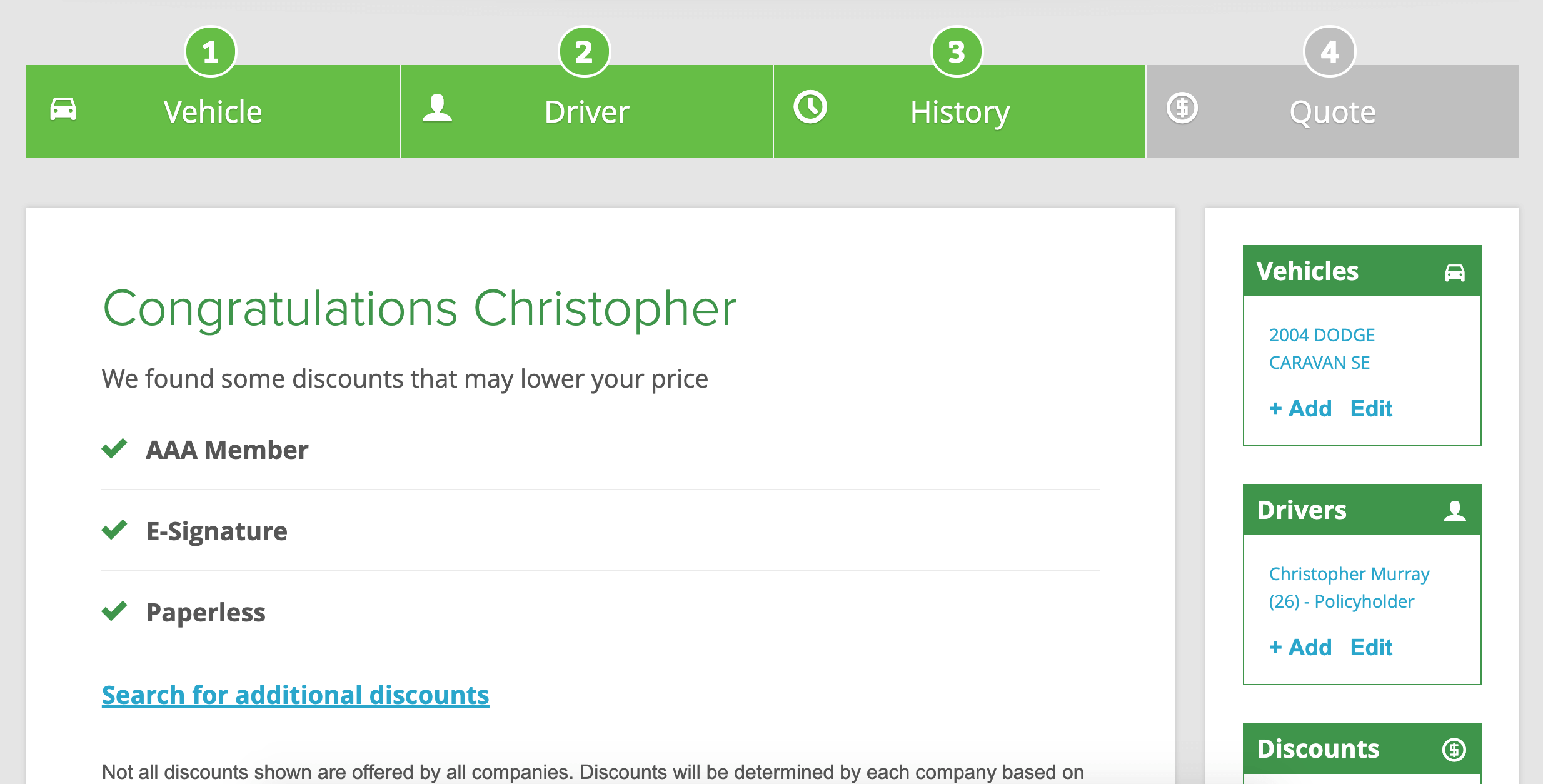

Based on the answers I gave, Compare told me upfront what discounts I’ll qualify for with most insurance companies.

To get an accurate understanding of all the discounts you qualify for, you’ll need to get a quote directly through the car insurance company.

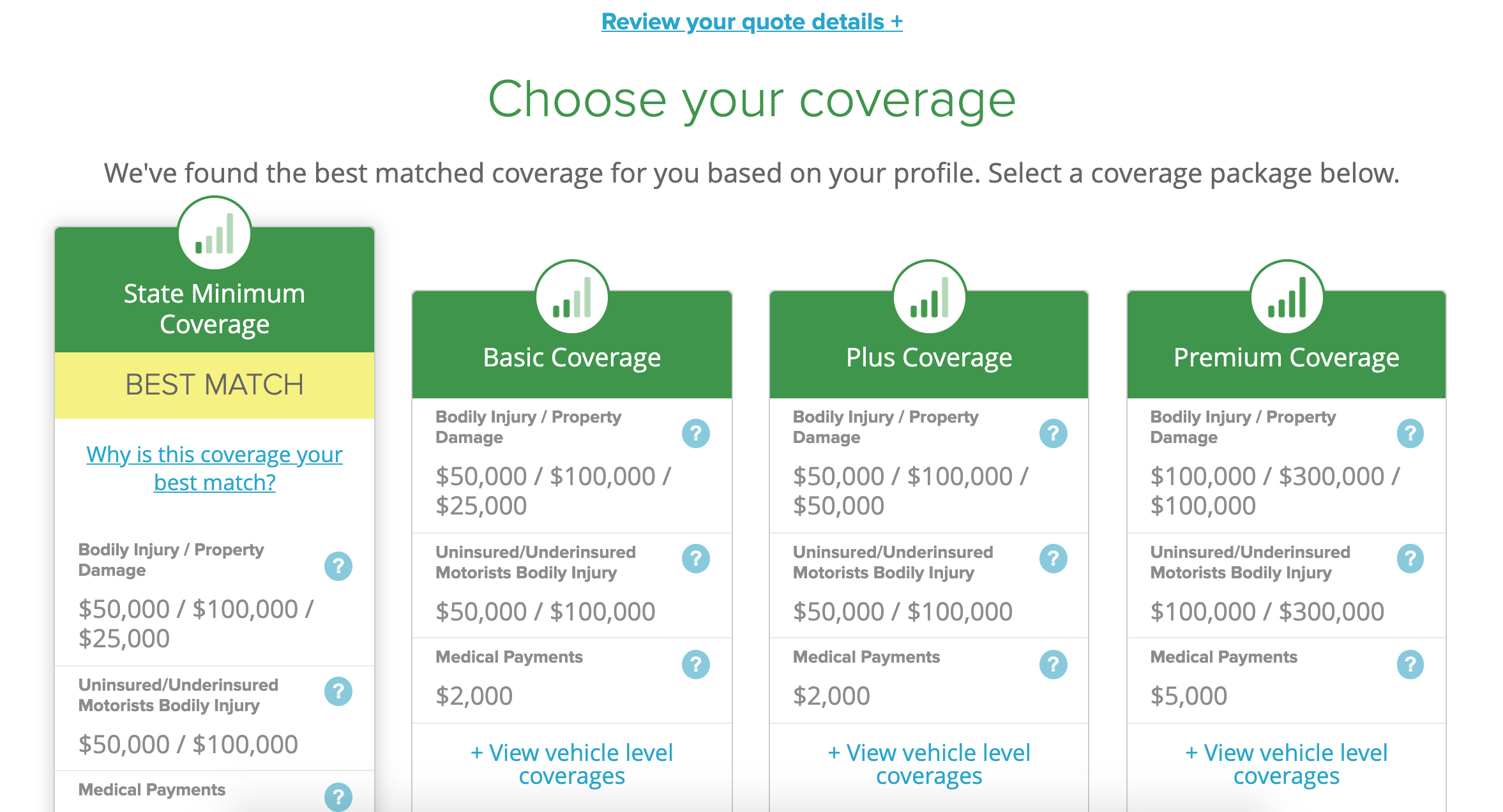

Finally, Compare asked me if I want to stick with the state minimum coverage or upgrade to a higher bracket and get more comprehensive insurance. I decided to stick with the state minimum for now (liability in my state).

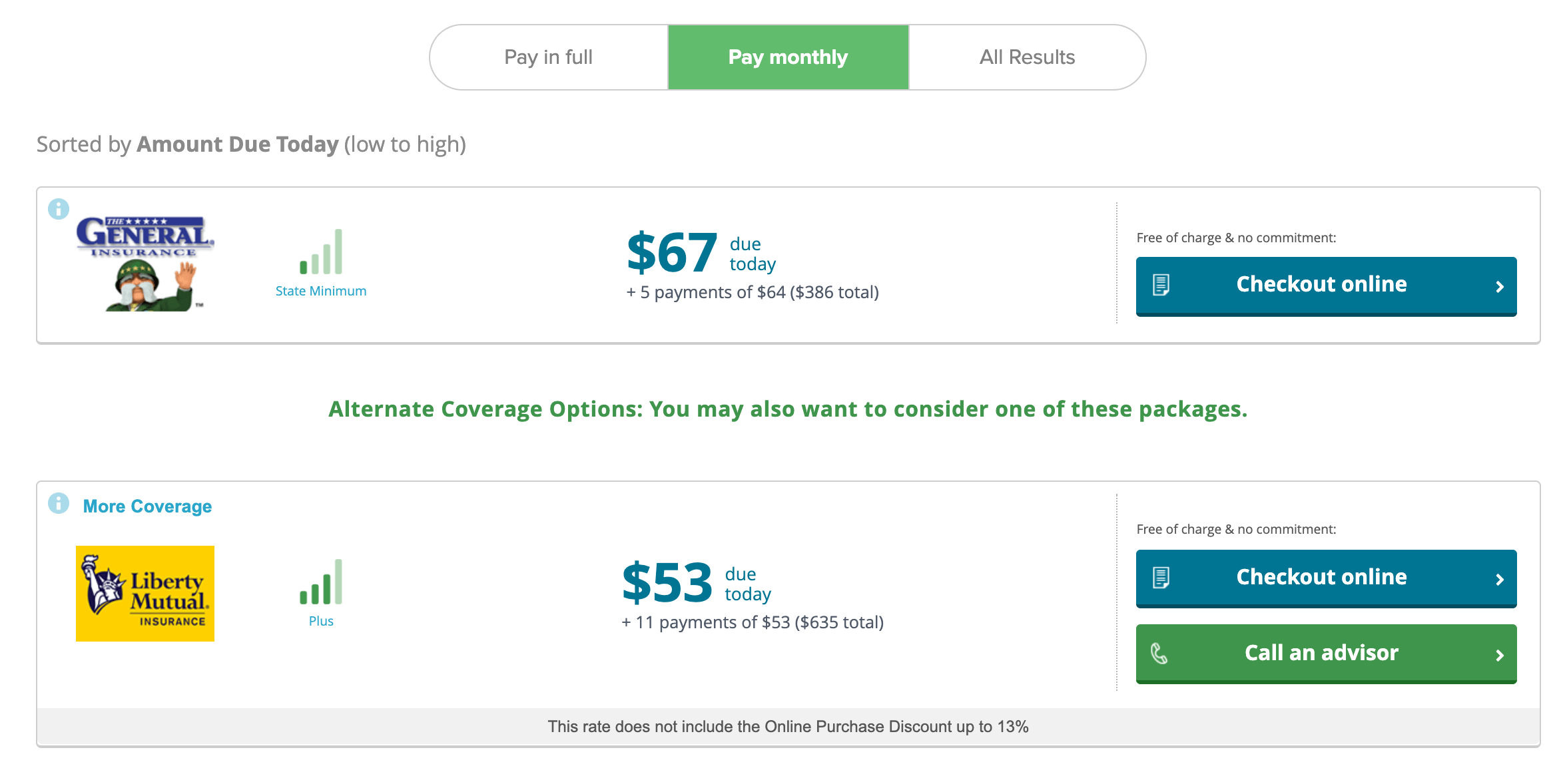

Finally, I got my quotes. The General and Liberty Mutual were my two cheapest options. Both are significantly cheaper than what I paid for liability insurance with Allstate. But, since I have such a long-running relationship with my Allstate agent, I qualify for discounts that neither The General or Liberty Mutual offer.

When I scrolled down, I was presented with many more insurance options. But to get quotes, I needed to go through each company individually.

How Do I Get My Insurance Rate To Go Down?

First, Look At What Determines Your Auto Insurance Rate

The rates that I got above may be significantly different than yours. In fact, yours will probably be lower. Auto insurance rates for a 26-year-old male are often the highest. Luckily, I’ve never been in an accident, I’m over 25, and I’ll be getting married soon, so my rates will drop significantly.

Your rate will be determined by the following factors:

- Your age

- Gender (women have lower rates than men)

- Marital status (married folks often have lower rates the unmarried folks)

- Where you live

- The car you drive

- How many miles you drive

- Your driving record

Call Your Insurance Company If You’ve Gone Through A Major Life Event

If you’ve experienced one of the following, call your insurance company and see if you qualify for a lower rate:

- Turned 25

- Got married

- Bought a house (you can often bundle your home and auto insurance)

- Improved your credit score

Become A Better Driver

If you don’t have the best driving record, you may be able to lower your rate if you take a defensive driving course. Although, if you go this route, make sure the cost of the course isn’t greater than the savings you’ll get from taking it.

Other Ways To Lower Your Rate

- Drive safely

- Avoid buying a sports car or extremely expensive cars

- Reduce your commute to work

- Improve your credit score

- Get a higher deductible

Common Car Insurance Terms

It’s important to understand some of the common language you find when learning about and shopping for car insurance. Here are a few of the words you’ll see the most:

- Umbrella policy–Insurance coverage that can protect you from lawsuits that may go beyond the limits and coverages of other policies.

- Deductible–The amount you must pay in the event of an accident before any payment is due from your insurance company.

- Claimant –The person who makes a claim in the event of an accident.

- Named driver policy–A car insurance policy that doesn’t provide coverage for an individual living in your household, unless the individual is named on the policy. If you and your spouse live together, but only your name is on the policy, any damage done by your spouse isn’t covered.

- Non-owner’s policy–Insurance coverage that offers insurance for those who do not own a vehicle but drive it. Typically, this includes your spouse or teenagers.

- Premium–How much you pay for your car insurance policy.

- Rider–An insurance policy addition that adds benefits to or changes the terms of a basic insurance policy.

- Claim–A request by you, the policyholder, to your insurance company for coverage or compensation for a covered loss (accident, damage, etc.).

- Policy lapse–When your policy is canceled due to nonpayment of the premium.

- Medical payments coverage–An addition to your insurance that will pay limited medical and funeral expenses if you, a family member, or a passenger in your car is injured or killed in a car accident.

- State-required minimum–The minimum amount of insurance your state requires (typically, liability).

Final Thoughts

Buying car insurance is incredibly complex. There are many different kinds of auto insurance and complicated terms that go with them. If you’re not clear on these definitions and types of insurance, you might get more than you need at a higher rate than you should be paying.

To get started, we recommend going to Compare.com, where you can see all your rates in one place. From there, you can pick what makes the most sense for your driving habits and your wallet.

Related Articles

- Get The Best Price On Life Insurance With Policygenius

- 6 Types Of Travel Insurance That Will Save You Money