The Ultimate Guide on how to negotiate anything from your salary to your bills, and level up your communication skills and self-confidence to boot.

Find out how to break into a High Paying Tech Industry Job and Unlock Remote Work and Benefits without going back to college or learning to code

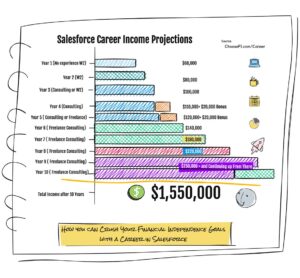

After Anita Smith lost her hospitality job, the ChooseFI community helped her double her income with a new Salesforce career.

Tori Dunlap talks about starting a business as a kid and negotiating your salary and her mission to help women earn their first $100k.