Stocks are shares of publicly traded companies that are sold on stock exchanges. There are over 3,500 publicly traded companies, from household names like Apple and Pepsi to smaller companies that you’ve probably never heard of.

There are two main ways to make money with stocks. One is by the stock appreciating in price. For example, if you buy a stock at $100 and it grows to $120, you’ve earned a 20% return on your money.

The other way that stock investors make money is by receiving investor dividends. A dividend is a regular payment that a company will pay its stockholders. Most stocks follow a quarterly dividend payout schedule. Many investors prefer dividend-paying stocks because they can provide a steady stream of passive income, separate from the stock’s overall price performance.

There are three main advantages of investing in individual stocks.

One of the advantages of stocks is that they’re a liquid investment. Stocks can be bought or sold at any time on stock market exchanges during open market hours or during after-market hours. As we’ll see later, that’s something that you can’t do with mutual funds.

Here’s the full definition of a liquid investment.

Another pro of stocks is that they come with advanced trading options that aren’t available to mutual fund owners, like the ability to make stop-loss and trailing-loss orders.

A stop-loss is a limit order that will only execute if your stock drops below a certain price.

For example, if you buy a stock at $100, you could set a stop-loss order at $95. If the stock ever falls to $95, the broker will immediately work to execute the order. Stop-loss orders are popular because they limit the investor’s risk.

However, they can only execute during regular market hours. Stocks can fall precipitously during pre-market hours. So by the time the market opens, your stock could have already fallen significantly below your stop-loss price. Therefore, it’s important to point out that stop-loss orders don’t eliminate risk entirely.

Here’s a full definition of s stop-loss order.

A trailing stop is an advanced stop-loss order. As opposed to setting a specific price as your stop-loss limit, you use a percentage. For example, you could set 5% as your trailing stop. In this case, any time that your stock drops 5% below its latest high, the sell order will execute.

Trailing stops can be more effective at limiting your risk. Here’s why. Imagine that you buy a stock at $100 and set a stop-loss of $95. That would be a loss of 5%. Sounds pretty good.

But then imagine that your stock grows to $150. Now if your stock dropped down to $95, that would mean it dropped over 35%! And that’s the inherent problem with stop-loss orders. Your risk grows as your stock appreciates.

But if you had a 5% trailing stop on your stock, it would have executed the order once the stock dropped to $142.50 (a 5% drop from $150). Trailing stops are great because they give you unlimited growth potential, with heavily defined risk. Personally, I never buy an individual stock without immediately creating a trailing stop order.

Here’s a full explanation of a trailing stop.

Stocks can be low-cost investments. Since you’re not buying a fund that needs to pay fund managers, there is no annual expense ratio…and you won’t be charged a sales load either.

Once you’ve purchased the stock, your expenses are virtually over.

Stocks are also a tax-efficient investing vehicle. While mutual funds can generate capital gains throughout your entire time as a shareholder, you won’t get hit with a capital gains tax on stocks until you actually sell your shares.

Listen: Capital Gains Harvesting

Okay, so those were the pros of stocks. But they also come with a couple of pretty significant downsides. Let’s take a look at what those are.

Stocks are the riskiest of the four investing options that we’ll be comparing in this guide. Your investing success rises and falls on the performance of one particular company.

If that company tanks, your portfolio will as well. That lack of diversification is the biggest downside to stock investing.

Yes, you could buy a few different individual stocks to provide some diversification. However, keeping up with the performance of ten or more stocks can be time-consuming.

And you’d still have far less diversity than the average mutual fund which typically holds hundreds of securities.

Related: Why Investing Conservatively Is Better

Traditionally, brokerages have charged a trading fee when investors trade stocks while allowing them to trade in-house mutual funds for free.

Trading fees are often less than $5. So for those who trade infrequently, that isn’t a big deal. But if you were making trades every month (or even more often than that,) your fees could add up quickly and hurt your overall return.

It should be pointed out that the events of the last year have made this a less common disadvantage of stock trading. The investing industry has undergone a massive shift as multiple brokers have removed their stock trading fees.

Currently, Schwab, TD Ameritrade, Fidelity, and Robinhood all offer free trades. And it’s probably only a matter of time before more brokers follow suit.

Related: How To Open Accounts With Vanguard, Fidelity, And Schwab

Remember how we said the biggest problem with individual stocks is their lack of diversification?

Well, mutual funds solve that problem. When you buy a share of a mutual fund, you’re actually buying little pieces of hundreds of underlying individual securities.

Whereas stocks can experience massive up and down swings, mutual funds tend to be a less bumpy ride for investors. So if you’re a conservative investor who wants to avoid market volatility, mutual funds can be a great choice.

In addition to the automatic diversification that they offer, mutual funds come with a few more benefits.

One of the biggest advantages of mutual funds is that you can match them specifically to your risk profile. The five most common types of mutual fund categories are:

The difference in each of these mutual fund categories mostly comes down to asset allocation. No matter your investing profile or goals, you’ll be able to find a mutual fund that’s a good fit.

Related: Asset Allocation When You Plan to Retire Early

Another potential advantage of mutual funds is that they often come with professional fund managers. And if you’re someone who’s new to investing, that might add a layer of comfort and security–but it also adds fees.

Finally, most mutual funds allow investors to buy “fractional shares.” And that can make it easier to invest specific dollar amounts on a consistent basis.

For example, let’s say a stock and mutual fund are both currently priced at $75 and you want to invest $100. With the stock, you’d only be able to buy one share and you’d have $25 left over. But with the mutual fund, you could typically buy 1.33 shares.

Being able to buy fractional shares is nice because you can literally put your investing on auto-pilot. With most brokers, you can set an automatic monthly trade at whatever dollar amount you choose.

So if you want to invest exactly $150 each month in a mutual fund, you can do that. And by doing that, you’d be taking advantage of dollar-cost averaging. In other words, when the mutual fund goes down, your $150 buys you more shares. And when the mutual fund goes up, it will buy you fewer shares.

Mutual funds have a lot going for them. But no investment product is perfect, and mutual funds are no exception. Here are two downsides you’ll want to be aware of.

One of the biggest cons of mutual funds is their cost. All mutual funds come with expense ratios. The expense ratios on actively managed mutual funds can be quite expensive, often ranging from 0.50% to 1.5%.

Many mutual funds also come with upfront sales loads, which can be up to 8.5% of the amount invested! So right off the bat, you’d be 8.5% in the hole. Put another way, you’d need your mutual fund to grow 8.5% just to break even!

Now most mutual funds don’t have sales loads that high. But many mutual come with loads between 3% to 5%. And, in my opinion, that’s just terrible.

Another potential drawback of mutual funds is that they aren’t quite as liquid as stocks. Unlike stocks, you can’t trade mutual funds during the open stock market hours. Instead, mutual funds trade once a day after the market closes.

So while you can get out of a sinking stock before it drops too far, you can’t do with that mutual funds. Even if you place a sell order at 10 a.m., your fund won’t actually trade until the end of the day.

Finally, mutual funds often come with investment minimums of $1,000 or more. With stocks, on the other hand, you only need to have enough money to buy one share. So if you don’t have a lot of money to invest, stocks (or ETFs) may be a better choice.

First, let’s clarify what an index is. To put it simply, an index tracks the stock price of a group of companies that have some common features. For example, the S&P 500 tracks the market capitalization (the stock price times the number of shares available to the public) of the 500 largest US companies. If the price of the stocks in those companies as a group goes up, the index rises. If the average stock price drops, the index falls.

Here is a more complete explanation of the S&P 500 index.

It’s important to note that you can’t invest directly in an index. It’s not an actual investment but rather information that is gathered and tracked. However, you can invest in an index fund. An index fund is a type of mutual fund that attempts to replicate an index as closely as possible. Whatever stocks the index is tracking are the stocks the fund will hold in the same proportions.

S&P 500 index funds are some of the most well-known and popular, but there are index funds that track every type of market index.

Some other examples would include:

And there are many, many more! Since index funds aren’t actively managed by fund managers, they are a form of “passive” investing.

Index funds have been the darling of the investing industry for over 40 years now. Here’s what makes them so great.

Since index funds don’t need to pay expensive fund managers to pick and choose the underlying stocks they tend to be much more cost-effective than actively managed mutual funds.

While the average mutual fund expense ratio is over 0.80%, the typical index fund expense ratio will be below 0.20%. This can make a huge difference in a fund’s performance over time.

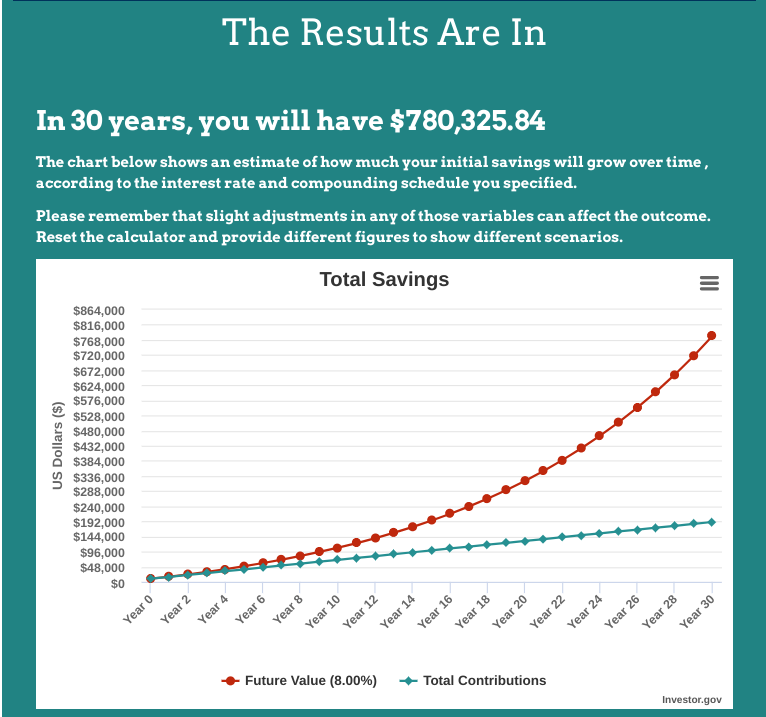

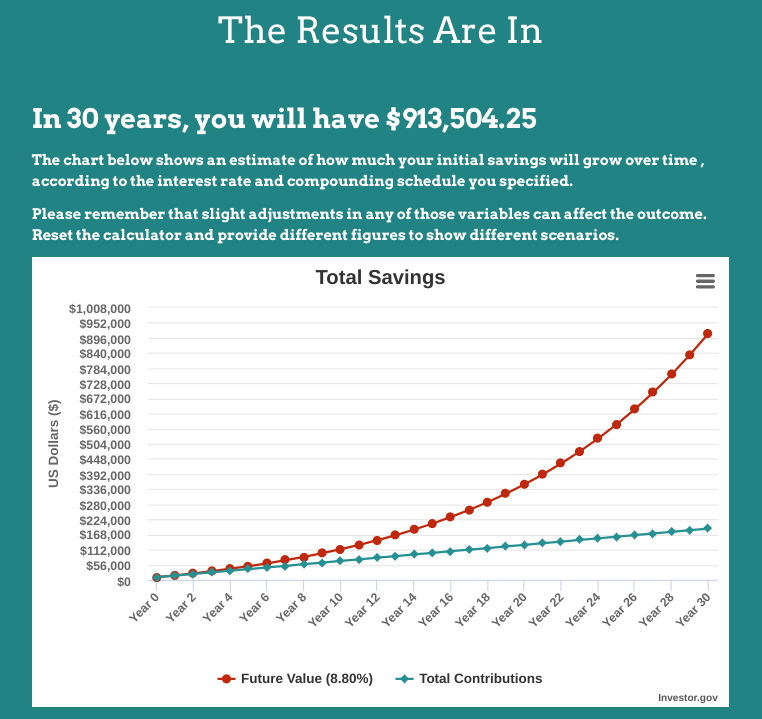

For example, let’s say that you invested $10,000 in a mutual fund and an index fund at the same time and you contributed an additional $500 each month. We’ll assume that both investments earned a 9% return. Finally, we’ll say that the mutual fund had an expense ratio of 1% and the index fund had an expense ratio of 0.20%.

In 30 years, your mutual fund would be worth over $780,000.

And the index fund? It would be worth over $913,000.

That’s a difference of $133,000! And this example perfectly illustrates why you need to pay attention to your mutual fund expense ratios.

Related: FIRE Essentials: Intro to Low-Cost Index Fund Investing

In our example above, we assumed that the mutual fund and index fund would earn the exact same rate of return. But advocates of actively managed mutual funds will cry foul. They’ll say, “But an actively managed fund’s expense ratio will pay for itself in better performance!”

But, surprisingly, that’s rarely the case. Index funds also tend to yield better returns than actively managed mutual funds. It turns out that “expert” stock pickers can’t beat the indexes either.

Over 82% of actively managed mutual funds have underperformed the S&P 500 over the past 5 years according to SPIVA Statistics. That’s a startling statistic.

To put it another way, 82% of the time actively managed fund owners are paying more for a lower return. That’s the definition of a bad deal.

Index funds share many of the same shortcomings as actively managed mutual funds. They also can’t be bought or sold until the end of each trading day. And many index funds come with investment minimums as well.

While index funds lack some of the features of stocks, they have very few downsides when compared to actively managed mutual funds. The only exception would be that you won’t be able to match an index fund to your specific risk appetite as you can with actively managed funds.

After John Bogle introduced the first index fund in 1975, it didn’t take long for investors to recognize their many advantages. And thus began a 40+ year passive investing revolution.

But index funds still had a few drawbacks, as outlined above. And, in 1993, a new investment vehicle called the exchange-traded fund (ETF) was introduced. It promised to offer the same advantages as index funds while removing some of their pain points.

Like mutual funds, ETFs are funds made up of pools of securities. But unlike mutual funds, ETFs are bought and sold on stock market exchanges just like stocks.

While there are some actively managed ETFs, most are designed to track market indexes, just like index funds. That can make them very affordable investments, which is one of the reasons why many robo-advisors use ETFs to build their portfolios.

Here’s a video that explains more about ETFs:

Related: M1 Finance Review: Completely Free Automated Investing

ETFs have taken the investing world by storm. ETF.com recently announced that total ETF assets had crossed the $4 trillion mark for the first time ever. Here are three reasons why ETFs have become so popular.

Since ETFs are traded on the exchange like stocks, they can be bought and sold at any time. You don’t have to wait for the market to close. And, as with stocks, investors can make advanced orders or trade during the pre-market and or after-market hours.

ETFs don’t come with investment minimums. As long as you have the funds to buy one share, you can get started with ETF investing.

This can make ETFs the best choice for beginning investors. With ETFs, investors can literally enjoy the diversification of an index fund with an investment amount of less than $100. That’s pretty amazing.

The cons of ETFs are similar to that of stocks. Some brokers still charge commissions on ETF trades. Although this has become less common over the past year.

It’s also less common for brokers to allow investors to buy fractional shares of ETFs (although some say that they’ll be adding this functionality soon). So if you’re a fan of dollar-cost averaging, an ETF may not be your best option.

Investing products have continued to improve over time. And, in many ways, it would appear that ETFs are the culmination of years of iterations. If you’re just getting started investing, an ETF may be your best choice.

However, you may already have a lot of money invested in your broker’s funds. And that’s fine. Mutual funds (especially index funds) are still a great investment product. As long as you’re paying a low expense ratio.

Finally, if you do decide to buy individual stocks, I would recommend only using a small percentage of your total investment capital. Stocks are simply too risky to place a high percentage of your retirement money in them. And if you do decide to buy stocks, consider using stop-loss or trailing-stop orders to limit your risk.