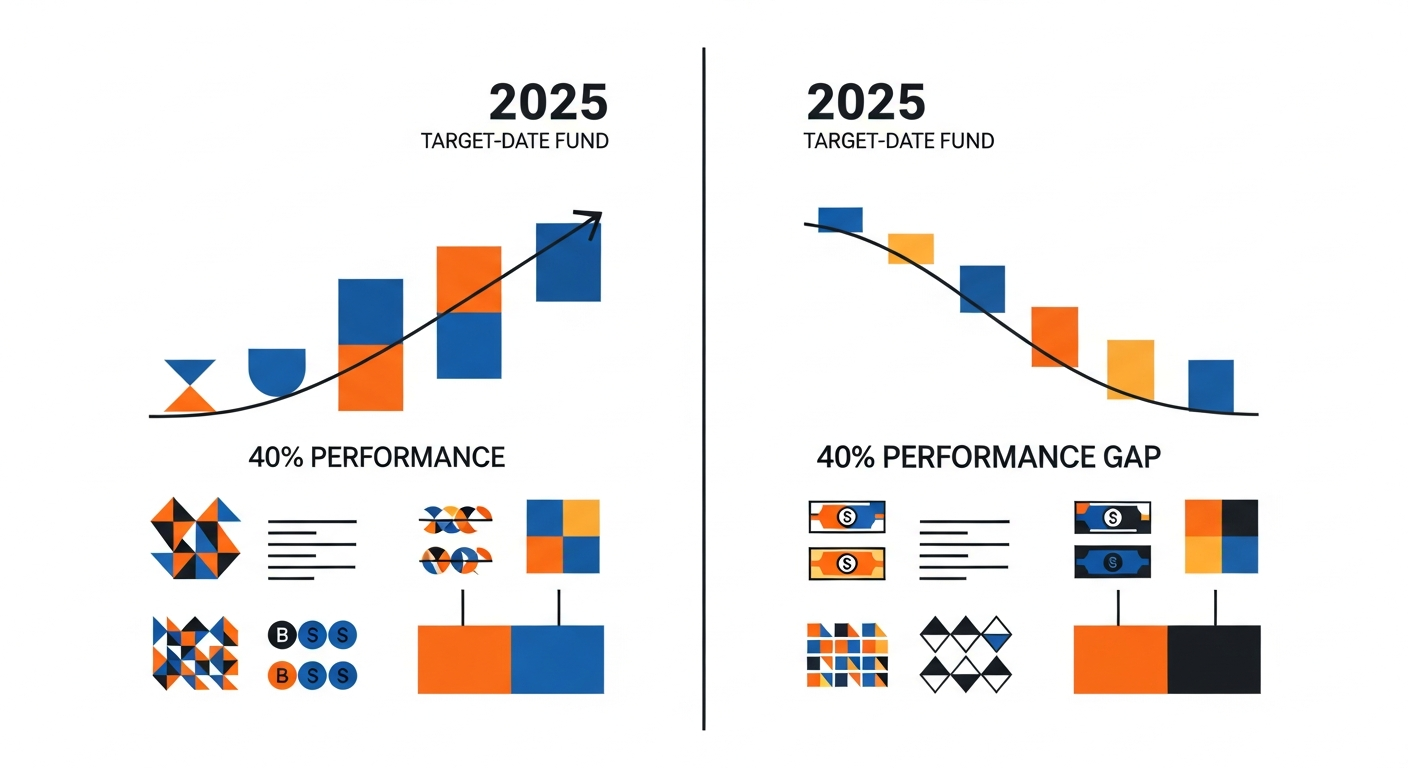

Most investors think they're buying the same thing when they choose a target date fund—but two people who bought 2025 target date funds 15 years ago could have 40% different returns today. Same target year, wildly different outcomes. The culprit? Fund families structure these "simple" investments in dramatically different ways, and most investors never look under the hood.

Key Topics Discussed

Passive Investing vs Active Financial Planning (00:03:30) Cody explains why you should be a passive investor but an active financial planner in your own life, noting that 95% of active investors underperform broad index funds over time.

Understanding Target Date Funds (00:08:15) How target date funds work as default 401(k) options, automatically shifting from aggressive to conservative allocations as retirement approaches along a predetermined glide path.

Surprising Differences Between Target Date Funds (00:18:45) The revelation that identical retirement target years can produce vastly different outcomes depending on fund family—differences in international exposure, bond types, and allocation strategies compound over time.

Comparing Fidelity, Schwab, and Vanguard Target Dates (00:24:00) Detailed breakdown of how three major fund families structure their target date index funds differently, with varying philosophies on diversification and risk management.

The Hidden Costs of Target Date Funds (00:32:20) Analysis showing target date index funds cost 35% to 400% more than purchasing underlying index funds directly. Fidelity's target date index fund, for example, is four times more expensive than buying Fidelity's component funds separately.

Static Allocation Funds Explained (00:38:10) Introduction to balanced funds that maintain constant allocations (like 60/40 stocks/bonds) regardless of your age or proximity to retirement.

Target Maturity vs Constant Maturity Bond Funds (00:42:30) Deep dive into how target maturity bond funds differ from traditional bond index funds—all bonds mature in the same year, converting to cash automatically without requiring you to sell anything.

The Seven-Year Bond Strategy (00:48:15) Cody's approach to determining bond allocation: calculate seven years of planned spending and hold that percentage in bonds. If you'll withdraw $40,000 annually from a $1 million portfolio, hold 28% in bonds ($280,000) and 72% in stocks.

Bond Ladders and Behavioral Finance (00:55:00) How target maturity bond funds overcome psychological barriers to spending in retirement by eliminating the need to "sell" assets—bonds simply mature into cash when you need it.

Simplicity vs Complexity in Portfolio Design (01:02:30) Cody shares his personal eight-fund retirement portfolio strategy, explaining why something that appears complex can actually feel simpler from a behavioral perspective.

Notable Quotes

Mike Piper, CPA (quoted by Cody Garrett, CFP®): "There is no perfect portfolio, but there are countless perfectly fine portfolios."

Rick Ferri, CFA (quoted by Cody Garrett, CFP®): "The perfect portfolio is the one you're going to stick with. Maintaining discipline is the hardest part of investing."

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

Join 25,000+ on the Path to FI

Free access to FI tools, forums, local groups, and 750+ episodes.

No password needed. Free forever.

Cody Garrett, CFP®: "Once you understand what a target date fund is, you no longer need one."

Cody Garrett, CFP®: "Investing is like a bar of soap. The more you touch it, the less there is."

Brad Barrett: "Success in personal finance and investing comes down more to behavior, vastly more to behavior than it comes down to any type of knowledge or intelligence."

Key Takeaways

- Review your 401(k) fund lineup and sort by expense ratio to identify the lowest-cost index fund options available to you

- If your 401(k) lacks low-cost index funds (under 0.10% expense ratio), contact your plan administrator to request they be added to the fund lineup

- Calculate how much money you plan to spend from your portfolio over the next seven years to determine your appropriate bond allocation

- Visit Morningstar.com and review the portfolio tab of any target date funds you currently own to understand their underlying holdings and allocation strategy

- Download Cody's 10-question portfolio design exercise at measuretwicemoney.com/ChooseFI to create a strategy you can stick with long-term

- Consider whether target maturity bond funds might help you overcome psychological barriers to spending in retirement

- Review your current investments to ensure you're not paying 2-4x more for a target date fund when you could purchase underlying index funds directly

Resources and Links Mentioned

Morningstar.com for fund research and portfolio analysis

ChooseFI Episode 556 with Rachel Camp, CFP®

ChooseFI Episode 194 with Frank Vasquez on the role of bonds

Oblivious Investor blog by Mike Piper, CPA

Bogleheads community

Vanguard Total World Stock ETF (VT), Vanguard Total Stock Market ETF (VTI), Vanguard Total Bond Market ETF (BND)

iShares iBonds, Invesco BulletShares, Vanguard Bond Builder Target Maturity ETFs, State Street My Income ETFs

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

FI Calculator

Travel Tools

Podcast

Local Groups

Forums

Book Club

Value Matrix

Debt Payoff

Workout Logger

Events

Join 25,000+ on the Path to FI

Free access to FI tools, forums, local groups, and 750+ episodes.

No password needed. Free forever.

Top Travel Card

Ready to unlock a world of free travel? Start with the Chase Sapphire Preferred® Card

$95 annual fee | Earn 100,000 bonus points

Best Card for Side Hustlers and Business Owners

Side hustlers! With the Ink Business Preferred® Credit Card you can earn free travel from your business expenses.

$95 annual fee | Earn 100,000 bonus points

Most Flexible Travel Card

The Capital One Venture Rewards Credit Card can be used to offset almost any travel expense.

$95 annual fee | Earn 75,000 Miles once you spend $4,000 on purchases within 3 months from account opening

ChooseFI has partnered with CardRatings for our coverage of credit card products. ChooseFI and CardRatings may receive a commission from card issuers.